U.S. Domestic Economic Items

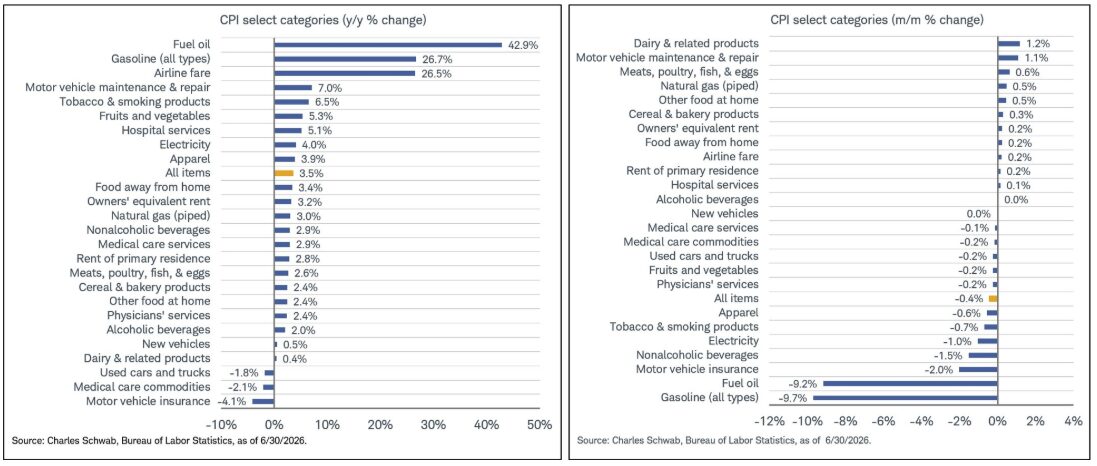

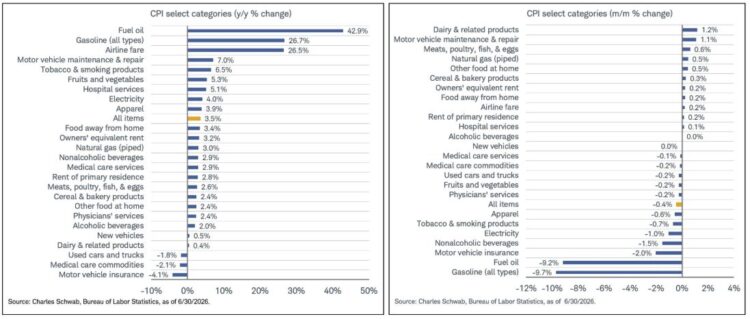

The CPI came in below expectations, and many categories have seen some deflation. With headline CPI coming in at 3.5%, it was still well above the Fed’s target rate of 2%, but it is headed in the right direction.

Looking at the chart below, a few things jump out:

- Most of the heavy inflationary items were still linked to oil and petroleum prices on a year-over-year basis, but those on the higher M/M list were inflating due to other factors.

- Of those not linked to the War in the Middle East, labor costs were a problem (such as in auto maintenance, which is both a labor and parts inflation issue).

Are the current disruptions in the Middle East nearing a conclusion, with the peak impact already behind us, or has the world already drawn down existing inventories and stockpiles of oil and other resources, and if the conflict continues deep into the fall, is the worst still potentially ahead of us?

China’s Growth Slows to a Crawl

Remember when it was asserted that any growth below 10% in China signaled a recession for that economy? This was recognition that a country with a population of 1.4 billion needed a robust growth rate just to keep enough of its population employed. When growth rates slowed to 7.0% or 6.0%, all sorts of alarm bells sounded, and the government took steps to boost growth – everything from expanding consumer access to direct subsidies.

The latest numbers from China are very distressing from a global growth perspective as well as for China. These are the worst growth numbers seen in decades.

Read more on how news, developments, and other global items are affecting your supply chain.