By Alex Stark

Mind the Head-Fake: Cooling Inflation That Isn’t, a Record Import Month That Shouldn’t Reassure You, the First Robot Strike, and the Case for Friction

A quick housekeeping item before we dive in. I’m heading out of town for a few days of R&R, so there won’t be a post next week. I’ll be back in the saddle the last week of July. As always, I deeply appreciate the readership.

The through-line this week is timing. Each of these stories is a number or an event that looks like one thing at a glance and turns out to be something else once you check what’s under the hood. Inflation “fell,” but look closer. Imports may hit a record, but for a reason that has nothing to do with demand. A factory strike over robots looks like a one-off and is anything but. And in customer experience, the thing everyone is racing to eliminate turns out to be worth keeping.

I’m still full-throttle into (global) football, so pardon my theory this week, “mind the head-fake.” There should be no doubt about the GOAT discussion. It’s Messi. All day. It should be quite a showdown in the final.

1. Inflation “Fell” in June. Look Closer Before You Celebrate.

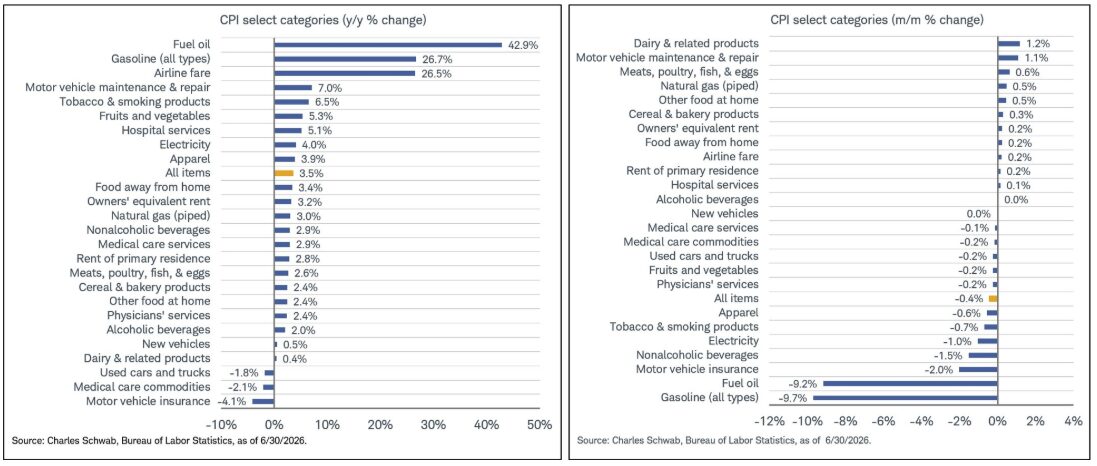

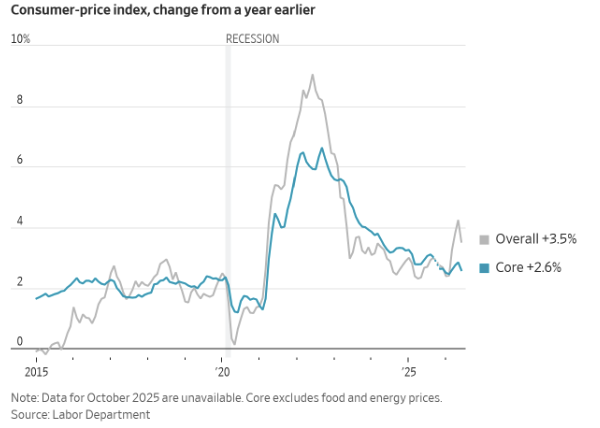

June CPI posted its biggest monthly drop since 2020. Per the report, headline inflation fell 0.4% for the month, the largest one-month decline since April 2020, and the annual rate eased to 3.5% from May’s 4.2%. Cue the celebration and good vibes, right? Except the drop was almost entirely energy, and the number underneath it barely moved.

The Number Under the Number

- Headline CPI: down 0.4% for the month, annual rate 3.5%, the first pullback in the annual rate since January.

- Core CPI (excluding food and energy): flat for the month, 2.6% annual, still above the Fed’s 2% target.

- The driver: a sharp fall in energy prices did nearly all the heavy lifting. Gas has been sliding for weeks. Food rose 0.2%, shelter rose just 0.1%.

- Still hot underneath: beef is up about 14% over the year on decades-low cattle supply, and tomatoes are up 20% on tariffs and weather.

There’s also a new hand on the wheel worth noting. Kevin Warsh has taken over as Fed chair, and at the June meeting, the committee struck a notably hawkish tone, signaling the rates would stay in place for the time being. Futures markets still lean toward a possible hike later in 2026, not a cut. So, a “cooling” headline did not change the Fed’s posture at all.

This is the leading-versus-lagging distinction I keep coming back to, with a timing twist. A single month driven by one volatile category is not a trend. Energy giveth, and energy taketh away. The core number, the one that really tells you where prices are heading, is stuck. One outlet called this report “a classic head-fake,” which is as good a summary as any.

The takeaway for operators is to avoid re-planning your pricing or wage assumptions around a single soft headline. Watch core, watch services, and watch what the Fed does rather than what the top-line print says. The relief at the pump is real. The underlying inflation picture has not meaningfully changed. And things are far from settled in the Middle East. All that uncertainty makes for choppy seas.

2. July Imports Just Hit a Record, and It Is Not Good News

U.S. container ports are on track to move 2.47 million TEUs in July, the highest monthly total ever recorded, according to the latest Global Port Tracker. That surpasses the 2.4 million set at the height of the post-pandemic surge in May 2022. A record. And almost none of it is demand.

It’s a Deadline, Not a Demand Signal

- A temporary 10% Section 122 tariff, imposed in February, lapses at 12:01 a.m. on July 24, and a heavier round is expected in early August. Buyers are pulling orders forward to beat both.

- The front-loading is expensive. Spot rates from Asia to the U.S. West Coast are up about 120% since mid-May; East Coast rates are up 85%.

- The hangover is already forecast. Volumes are projected to fall to 2.22 million TEU in August and under 2 million by September. The peak is a pull-forward, and the second half pays for it.

- Credit where due: the ports are absorbing the surge without gridlock. Even at record volume, LA and Long Beach reported almost no ships at anchor over the July 4th weekend. The pinch point this time isn’t congestion. Its rates and surcharges.

This is the direct sequel to the “Christmas in July” front-loading I wrote about two weeks ago. Back then, it was a pattern. Now it’s a record. And a record manufactured by a deadline is not a sign of strength. It’s borrowed volume, pulled forward, and at a premium. Read the July number as what it is. It’s fear of a tariff cliff, not confidence in the consumer.

The practical move is straightforward. If you have deadline-sensitive freight, move it now. Then plan for a genuinely soft Q4, because a big chunk of the fall’s volume is already sitting on the water in July. Don’t let a record month set your Q4 capacity assumptions. This is exactly the flexible-warehousing, plan-for-the-whipsaw environment I keep describing, and it’s the work we do.

3. A Strike Over Robots Just Shut a Car Factory for the First Time. Remember the Date.

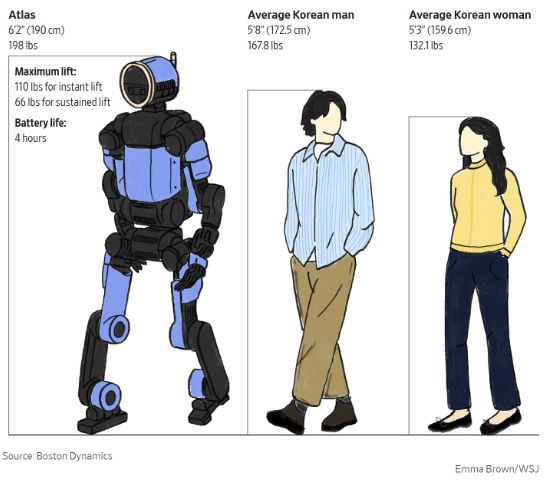

Hyundai’s auto workers in South Korea staged a partial strike this week. Per the WSJ, it’s the car industry’s first factory work stoppage tied to humanoid robots. When Hyundai unveiled its Boston Dynamics “Atlas” humanoid worker in January, union members said it would never step onto the production line. This week, they backed that up by walking off the job.

This Is Not an Isolated Event

- Hyundai plans to bring Atlas into U.S. factories starting in 2028, beginning with repetitive logistics work and moving to assembly by the end of the decade.

- GM installed about 50 collaborative robots at its Factory Zero plant in Detroit shortly after laying off more than 1,000 workers there. Toyota is deploying humanoid Digit robots at a plant in Ontario. BMW is expanding a humanoid pilot in Leipzig. In China, UBTech has put dozens of Walker robots into a Zeekr EV plant.

- The economics are blunt. After the 2023 UAW contract, GM estimated labor costs would rise by roughly $500 per vehicle. Vehicle assembly already takes 50 to 70 percent fewer labor hours than it did in the 1980s, and that number continues to fall.

As one analyst put it, in a line that stuck with me…

Robots do not renegotiate every four years.”

Two weeks ago, I wrote about AI CEOs walking back their job-apocalypse rhetoric. This is the counterpoint on the factory floor, where the story is not softening at all. The useful frame is the one I keep landing on. The question isn’t whether automation eliminates jobs or creates them. It’s who captures the gains, and whether workers have a seat at the table when that gets decided. That’s exactly what the Hyundai and the Korean auto employees are about.

UAW president Shawn Fain framed it as “a fight for humanity,” and whatever you make of the rhetoric, the 2028 UAW contract talks are shaping up as the most consequential in a generation.

Here’s the takeaway for operators. This is the first factory stoppage over humanoid robots. It will not be the last. If your operation is automating any repetitive physical work, the technology question is the easy part. The workforce-transition question (who gets retrained, who gets redeployed, how the gains get shared) is the hard part, and it’s the same lesson as the Kimberly-Clark “citizens, translators, wizards” piece from a couple of weeks back. Reskilling is the whole ballgame. Handle it thoughtfully now, or handle a harder version later when there is potential labor conflict.

4. In Customer Experience, Not All Friction Is Bad

I genuinely enjoyed this article from CX Dive this week. It was a refreshing counterweight to the strip-out-all-the-friction gospel everyone has been preaching. For years, the CX (NPS) mantra has been to eliminate every possible point of friction. This piece argues that’s a misread. Some friction is worth keeping.

The whole thing comes down to a single question:

Does the friction serve the customer, or the business?”

Bad friction serves the business at the customer’s expense. One click to subscribe, ten steps, and a phone call to cancel. Good friction serves the customer. Examples would include a confirmation step before an irreversible action, a moment that builds ownership or trust. The example that stuck with me is Trader Joe’s. By modern standards, it has plenty of “friction.” No loyalty app, no online ordering in most locations, and a smaller curated selection. And it’s one of the most beloved retailers in the country. As the source put it, you don’t have to buff every last bit of friction out of an experience to have a great one. Sometimes the friction is the experience.

This threads back to the Tillster loyalty piece from April and the Duluth-hands-Amazon-the-keys story from two weeks ago. Convenience is powerful, but convenience is also the most commoditized thing you can offer, because someone with 80,000 trailers can always be more convenient than you. Thoughtful, customer-serving friction, the kind that builds trust and ownership, is harder to copy than speed. In a race to zero friction, the differentiator may be the friction you intentionally keep.

The B2B translation is that the lesson is not “add hassle.” It’s about being deliberate about which steps in your customer experience are worth keeping human, slowing down, confirming, or having a conversation. The order confirmation that a person reads. The proactive call before a problem becomes a crisis. Those are “friction” items and trust-building experiences. AI can strip out the friction that annoys. The true art is knowing which friction to protect.

Mind the Head-Fake

Four numbers, four possible misreads waiting to happen. Inflation “fell,” but only energy moved, and the Fed did not blink. Imports hit a record, but a tariff deadline built it, and the fall will pay for it. A robot strike looks like a one-off and is really the first page of a long chapter. And the friction everyone is racing to delete turns out to be worth keeping in the proper places.

A single month, a single deadline, a single data point rarely tells you what it appears to be at first glance. The discipline is to check the timing and the composition underneath the headline before you act on it.

Where are you seeing a head-fake in your own numbers right now? And as I mentioned up top, I’m off next week for some PTO. I trust I’ll see you in a couple of weeks.

Bonus #1: Can a Prettier Data Center Cool the Backlash?

There seems to be no end to the stories about data centers. Do they add to noise pollution? Increase utility bills? I’ve been reading that even as usage keeps climbing, the two dominant players, OpenAI and Anthropic, are reportedly spending more on operating costs than they earn in revenue. There are many questions, concerns, and ideas about what this future will look like, and construction is being blocked outright in some places.

This article, originally published in the WSJ, caught my eye. Can a better-looking, better-integrated data center ease the community backlash I wrote about back in April? Maybe there’s something to the harmony between the building and the surrounding communities. What do you think?

Bonus #2: One of These Things Is Not Like the Other

Staying on AI, here’s a fun diversion I discovered. It makes me think of the great Sesame Street segment, “One of These Things is Not Like the Other.” This Google Arts and Culture experiment asks whether you can spot the phony from the real images. Given everything in this week’s post, it felt like a fair test of whether any of us still can. I felt pretty good that (for now) I was able to identify the impostors.

One Last Thing… Look Out for Each Other

Heavy smoke from wildfires in Canada is moving into the Midwest and Northeast. Be mindful of poor air quality, especially for sensitive groups such as children, older adults, and people with heart or lung conditions. Check on the folks around you who may be affected.

Look out for each other.

Remember, it costs nothing to be kind.