By Alex Stark

Nobody’s Waiting for Normal Anymore: The End of the Freight Downturn, the Real Story in Retail Sales, and the Lasting Lessons of Hormuz

Summer is officially here, the World Cup (and, of course, my beloved Phillies) have my evenings-TV-watching booked, and I keep waiting for the economic news to settle into a nice, lazy seasonal rhythm. It is not cooperating.

I spent the majority of this week traveling. In between meetings, airports, and sitting on the tarmac, I read four things that, taken together, finally convinced me of something I’ve been circling for a while. Nobody is waiting for normal anymore. The companies doing well right now have stopped trying to get back to the pre-pandemic world of 2019 and started building for whatever this actually is. There’s something a little freeing in that, once you accept it.

Four things to share. Let me know what you’re seeing.

1. U.S. Companies Have Stopped Waiting for Supply Chains to Return to Normal

A WSJ piece this week, reinforced by the just-released 2026 State of Logistics Report from Kearney and Penske for CSCMP, makes it official. Volatility has moved from a temporary disruption to a permanent feature of the operating environment. Stability can no longer be taken for granted, and resilience is becoming more important than pure efficiency.

The Numbers Behind the Shift

- U.S. business logistics costs hit roughly $2.4 trillion in 2025, about 7.8% of GDP. That’s actually down from $2.6 trillion and 8.7% the year before, so costs eased even as uncertainty climbed.

- The report names five structural forces reshaping the environment: asymmetrical global growth, tightening financial conditions, geoeconomic realignment, labor and productivity constraints, and energy price volatility.

- On behavior, a recent survey found 77% of supply chain leaders have already shifted sourcing away from China toward tariff-neutral countries, and 87% are increasing buffer inventory to hedge against volatility.

For four years, “when will things get back to normal?” was the most common question in this industry. The answer that has finally arrived is the one nobody wanted. They will not, and that is now the plan. The winners stopped waiting and started redesigning.

It’s worth being honest about the cost, though. Building for resilience rather than pure efficiency isn’t free. Buffer inventory ties up capital. Nearshoring rarely lowers your unit cost. Diversified suppliers are harder to manage than a single source. The companies making these moves aren’t doing it because it’s cheap. They’re doing it because the last four years taught them exactly what the absence of resilience costs, and that cost turned out to be much higher.

This is the same argument I’ve been making for two months about dedicated capacity and asset-based carriers, just viewed from 30,000 feet. Resilience over pure efficiency is the entire case for owned equipment and deep carrier relationships. It’s the business we’re in.

2. The Freight Recovery Is Real. Read the Fine Print.

A Transport Topics piece on the same Kearney report digs into the freight and transportation specifics, and the headline is genuinely good news with a genuinely important asterisk. The longest freight downturn in industry memory appears to be ending. But the recovery is being driven by capacity exits, not by a surge in demand.

What the Data Actually Says

- The ATA For-Hire Tonnage Index rose 2.6% in the first four months of 2026 versus the same period in 2025.

- The report states that higher rates are mainly attributable to capacity leaving the market, not freight demand rising.

- The warning that stuck with me: 2026 will not reward broad market assumptions.

Korhan Acar, the lead author, had the line of the week:

Today, the fog has become an operating environment.”

Geopolitical uncertainty, trade realignment, energy volatility, inflationary pressures, and rapid technological change have combined to create a state of persistent disruption. The fog isn’t lifting. It’s just where we work now. I thought I would have left the fog of the West Coast behind when I came back East at the end of this week.

One genuinely useful insight the report highlights is that less-than-truckload (LTL) is a segment to watch. LTL covers shipments roughly 5,000 to 27,000 pounds, or six to 18 pallets. It lets shippers avoid paying for unused trailer space while sidestepping some of the handling complexity that comes with LTL. It works best when a carrier or broker can combine compatible freight, build efficient pickup and delivery sequences, and meet service commitments. That’s an operational competence story, not a rate story, and it’s exactly the kind of capability that separates partners worth keeping from vendors worth shopping.

Here’s the part shippers need to sit with. A recovery driven by shrinking supply behaves very differently from one driven by growing demand. If you’re waiting for rates to soften once demand “normalizes,” you’re watching the wrong variable. Capacity is not returning quickly for the regulatory and demographic reasons I’ve written about over the past several weeks. Lock in your strategic lanes with longer contracts. Don’t treat a supply-driven recovery as a cyclical blip to wait out.

3. Consumers Kept Spending in May. Look Closer at the Why.

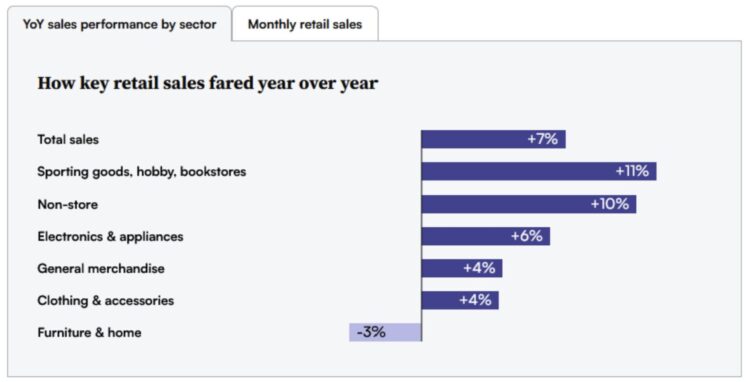

May retail sales from the Commerce Department came in at $763.7 billion, up 0.9% from April and up 6.9% from a year ago. On the surface, a resilient consumer. The honest read is the one Retail Dive landed on: consumers kept spending despite putting more toward gas, and they got less for their money.

The Catch in the Numbers

- Total retail and food services: $763.7 billion, up 0.9% month over month, up 6.9% year over year.

- Non-store retail (mostly e-commerce) was up 12.2% year over year, still the engine of the whole figure.

- The asterisk: these numbers are not adjusted for price changes. With May CPI at a three-year high of 4.2% (which I wrote about last week), a real chunk of that “growth” is inflation, not incremental real buying.

This is the same split I flagged a few weeks ago in the stock-market-versus-sentiment story. The top-line number looks healthy. Underneath, consumers are working harder to stay in place, spending more dollars to bring home a similar or smaller basket of goods. Gas took a bigger share of the wallet in May. Nominal up, real closer to flat.

For anyone planning freight volume based on retail demand, that distinction matters enormously. Dollars moving up while units move sideways means your warehouse throughput and transportation volumes may not track the headline retail number at all. Plan against units, not dollars. The consumer is not collapsing. The consumer is also not as strong as $763.7 billion makes them look. Both are true, and operators who read only the headline will misjudge their demand.

4. Five Things the Hormuz Crisis Taught Us, and One We Should Have Already Known

The WSJ ran a retrospective this week on what the Strait of Hormuz crisis taught us about the global economy. Given how much of this year’s writing has touched the Iran war’s downstream effects (diesel, helium, fertilizer, the Saudi truck convoy), it feels like the right one to close on. It’s the structural lesson sitting underneath almost every other story of 2026.

The Lessons Worth Keeping

- Chokepoint concentration is the hidden architecture of the global economy. Before the crisis, the Gulf supplied roughly 20% of seaborne oil, about a third of the world’s helium, and a meaningful share of ammonia and fertilizer. One narrow waterway, an outsized share of critical inputs.

- The damage was never just oil. The crisis rippled into semiconductors, aerospace, automotive, and AI infrastructure through helium, petrochemicals, and fertilizer. The second-order effects mattered more than the headline crude price.

- Alternatives exist, but they are slow and expensive. The Saudi East-West pipeline and that 3,500-truck convoy I wrote about in May proved a workaround was possible. They also proved how much effort and cost it takes to route around a single point of failure.

- Efficiency was never free. It was unpriced risk. The system optimized for cost and speed for decades precisely because the chokepoint kept working, right up until it didn’t.

- The vulnerability is permanent, not pandemic-specific. COVID got blamed for a fragility that was actually structural. Hormuz proved it was baked into the design, not a one-time shock.

The One We Should Have Already Known

Every operation has a Strait of Hormuz.

I wrote that line back in April with the helium piece, and the crisis has only made it harder to ignore. The single-source dependency. The one supplier. The one lane. The one chokepoint you’ve never stress-tested because it has always just worked. That’s the risk worth mapping before the next disruption, not after.

The efficiency we spent decades optimizing for was quietly borrowing against a risk we never put on the books. Hormuz was the margin call.

Four Stories. One Pattern.

For four years, we treated disruption as an interruption, something to endure until normal returned. This week’s reading shows the industry quietly conceding that the interruption was the new baseline all along. Companies have stopped waiting. The freight recovery is real but supply-driven. Consumers are spending more to get less. And Hormuz showed us, once again, that the efficiency we spent decades chasing was borrowing against a risk we never wrote down.

The lesson isn’t panic. The lesson is stop waiting. Map your chokepoints. Price your risk. Build for the weather you’re experiencing, not the weather you wish you had.

What are you no longer waiting for to return to normal? I’m genuinely curious.

Bonus #1: American Football Has Nothing to Worry About

World Cup fever is upon us in North America. Close to my corner of the supply chain world, fans from Ecuador, Brazil, and (maybe the favorites to win the whole thing) France are descending on the “Philadelphia Stadium.” As a too-proud Birds fan, to me it will always be the Linc. Sorry, FIFA.

Maybe with another win (or two), the U.S. Men’s National Team will start to claim a larger share of the national headspace. I saw a graphic this week comparing the audience and dollars behind the NFL to domestic soccer, though, and I don’t think American football has anything to worry about just yet. The gap is still a canyon. Still, it’s a fun few weeks to be a soccer fan in this country, and the energy in Philadelphia has been genuinely great.

Bonus #2: The Vuvuzela, Remember That?

Deep-diving a bit on soccer this week, I read a fun story about the much-maligned vuvuzela. Remember that thing? The buzzing… you’ll know. The 99% Invisible episode tells the whole story.

The vuvuzela became the global symbol of the 2010 World Cup in South Africa, that constant 120-decibel drone you could not escape on any broadcast. It drew endless complaints, nearly got banned by FIFA, and somehow turned into an unlikely manufacturing story along the way, with plastics shops scaling up overnight to meet sudden world demand. There’s a quiet supply chain punchline in there for those of us who think about that sort of thing. A single cheap plastic horn became the sound of an entire tournament, then mostly vanished. Worth the listen.

You’re welcome.

PS: We still have one in our basement. I need to make sure the kids don’t find it.

Remember, it costs nothing to be kind (to our ears, for sure).