By Alex Stark

What Summer Challenges in Logistics, Rare Earth Materials, Berkshire’s Housing Bet, and a New Wharton Study on AI Are Trying to Tell Us

It’s finally feeling like summer in my corner of the supply chain world. Sunny skies, consistently warm temperatures, and moderate (to now, no) rain have made everything perk up. A few days ago, while out driving, I noticed that all the forests covering the mountains where I live are fully green. No more brown until November. There’s a moment every spring when the season really commits, and we’ve hit it. About time. Bring on summer in all its glory.

The news this week wasn’t quite as cheerful as my view. Four stories caught my attention, and they all seemed to circle around the same idea. A lot of what we built our businesses around during the past 30 years is being quietly tested by everything happening at once. Cheap fuel. Stable suppliers. Plentiful (and relatively inexpensive) labor. Accessible housing. Customers who were delighted when products arrived faster than expected. Each of those assumptions is showing wear right now.

I’d love to know what you’re seeing.

1. The Summer Freight Picture Wasn’t Built for This Much Diesel Volatility

A SupplyChainBrain piece this week lays out the biggest challenges facing logistics operators heading into summer, and the picture isn’t pretty. Diesel prices are up nearly 50% since the war in Iran started in late February. Some experts say it could take a year before prices resettle.

Operators are already adapting in real time. Shipment data from January through April of 2026 shows that load density (the average number of orders per consolidation load) increased 19% as carriers worked to maximize every mile traveled. That’s the right move. It’s also a sign that an industry is quietly absorbing more costs than the headlines suggest.

The Visibility Problem Hiding Underneath

The article makes a point I’ve been thinking about for weeks. Despite advances in technology, many warehouses and distribution teams continue to rely on disconnected systems and manual processes to manage inventory and workflows. When disruptions happen, teams struggle to access accurate, real-time information quickly enough to make informed decisions.

Resilience right now is largely a function of two things. One, how integrated your systems are, and two, how flexible your network is. Both should be assessed honestly. Both can be improved. Neither happens automatically.

And I’d add a third. Do an audit on how deep your carrier relationships go. Asset-based operators with owned equipment and owned drivers have a meaningfully different cost structure when diesel spikes than a spot-market operator does. You can pay for that resilience now or pay for its absence later. Our take on what that looks like in practice is here.

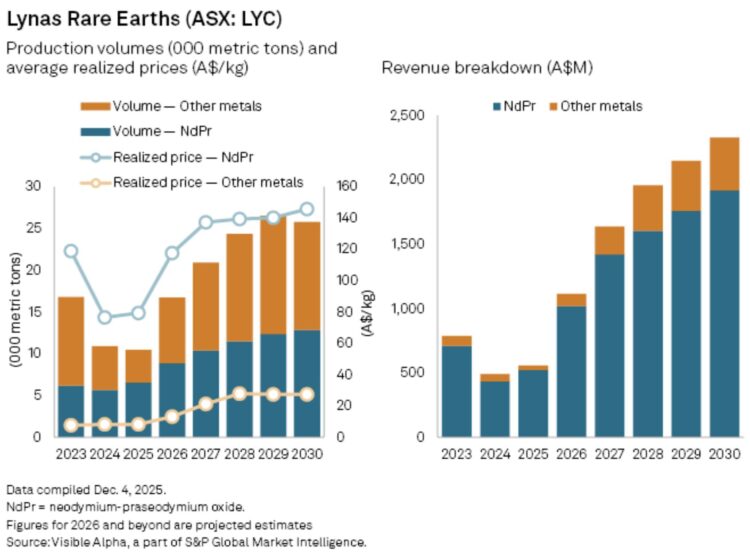

2. Does the World Need Chinese Rare Earths? Not Necessarily, Say These Companies.

A WSJ piece this week pulled together something I’ve been reading about off and on but hadn’t fully appreciated. A real ecosystem of non-Chinese rare earth suppliers is emerging, and it’s moving faster than I expected. Bloomberg Intelligence is now forecasting that China’s share of the rare earth magnet market could fall from roughly 90% to 69% by the end of the decade.

What’s Happening

- MP Materials in California and Lynas Rare Earths in Australia are the two leading non-Chinese suppliers. Both are scaling significantly.

- Recent U.S. policy moves, including a $400 million investment in MP Materials and Apple’s $500 million recycling partnership, are accelerating the build-out.

- The Lynas supply chain itself is a case study in coordinated decoupling. Concentrate from Mount Weld in Australia, refined in Malaysia, metalized in Japan, finished products across East Asia, with the U.S. as the largest end user. Multiple countries, with multiple stops, are producing alternative supply chains.

- U.S. policy could stimulate 29,600 metric tons of new NdPr supply outside China this decade, according to Bloomberg.

The proper reading of this isn’t “decoupling is happening.” The right reading is that decoupling takes a decade and a lot of capital, and most companies haven’t started yet. Japan has been working to reduce its dependence on rare earths for 15 years, yet China still accounts for about 76% of its supply.

This is the geopolitical version of the helium story I wrote about back in April. Every operation has a single-source dependency; it likely hasn’t been fully mapped. Rare earth metals and their production are just the version of that same story.

If your operation depends on a critical input that comes predominantly from one country (e.g., rare earths, lithium, semiconductors, specialty chemicals, or even certain agricultural commodities), what does your alternative pathway look like? Most operators I talk to haven’t run that exercise in detail. The companies that come out of the next disruption ahead are the ones doing the unsexy supplier-mapping work right now.

3. Berkshire Just Doubled Down on the American Dream of Homeownership

Berkshire Hathaway acquired Taylor Morrison this week, one of the largest homebuilders in the country, with a Sun Belt-heavy portfolio across Texas, Florida, Arizona, the Carolinas, and Georgia. Combined with Clayton Homes (Berkshire’s existing manufactured housing arm), Berkshire now has serious skin in both the affordable and the production-home segments of the U.S. housing market.

It’s a contrarian bet at first glance.

The Numbers Pulling in the Other Direction

- More than 70% of Americans say they’re concerned about housing affordability.

- The national median single-family home price is roughly $400,000.

- 30-year mortgage rates have stayed above 6% for months.

- There’s an estimated housing supply shortage of 4 million units in the U.S.

- Recent surveys suggest younger generations are reconsidering homeownership entirely. Only 8% of Gen Z renters define the American Dream as owning a home.

Warren Buffett’s career has been built on betting on the long-term continuity of American consumer behavior. Sometimes those bets look obvious in retrospect, like insurance, consumer brands, even railroads. Sometimes they look contrarian at the time. This is the latter. The question is whether the dream of homeownership is genuinely fading, or just temporarily under pressure. Berkshire is putting capital on the side of “temporarily.”

There’s a supply chain angle here worth noting. Housing is one of the most freight-intensive sectors in the U.S. economy. Every new home represents tens of thousands of pounds of materials moved from suppliers to job sites. If Berkshire is right that a homeownership resurgence is eventually coming, the building products supply chain is positioned to be a major beneficiary. If they’re wrong, housing-adjacent freight categories are facing a structural headwind for a while.

Either way, it’s worth watching what Berkshire does over the next 24 months. They tend to know things the rest of us don’t. I’m not saying that their strategy will be 100% accurate, but it’s hard to argue with their success.

4. Is AI Killing User Experience?

A new piece from Knowledge@Wharton this week reframes the AI-and-UX conversation in a way I hadn’t seen before. The argument from Scott Snyder and Mike Welsh:

The question is not really whether AI is killing user experience. The better question is whether AI is exposing the parts of UX that organizations have been treating as optional.”

That seems like a practical question to ask.

What the Data Shows

- Only 17% of consumers believe their AI-influenced experiences are actually getting better (Medallia, March 2026).

- More than 60% of consumers lack confidence in how businesses are using AI to interact with them (Pega, February 2026).

- AI can now generate customer journeys, personas, screens, content, and front-end code in hours rather than weeks. The bottleneck isn’t speed anymore.

The Speed Trap

The article’s writers, Scott Snyder and Mike Welsh, call it the speed trap. Teams can move from idea to artifact faster than ever. They can test more options. They can ship more iterations. None of that guarantees they’ve understood the end user’s moment, the context around it, or the emotion underneath it. AI accelerates the making. It doesn’t accelerate the understanding.

There’s a real lesson here for B2B operations that are leaning into AI-driven customer interactions. The operators winning aren’t the ones using AI to scale every customer touchpoint. They’re the ones using AI to take the friction out of the boring parts so humans can spend more time on the parts that matter. The order acknowledgment, the routing confirmation, the inventory report, are all good places for AI. The relationship management, the problem solving, the difficult conversation about a missed delivery. Those are still human jobs.

I love this quote from the piece: “The future belongs to teams that use AI to deepen understanding, not avoid it.”

Snyder and Welsh outline a practical approach with recommendations for business leaders.

- Investment made into UX will be a strategic asset for organizations. The volume of AI-generated project output will only increase. Using stronger UX judgment will make better sense of that output.

- Training teams to work alongside AI is paramount. The goal is not fluency alone, however.

- AI experiences should have human oversight designed into the architecture from day one.

- AI can accelerate output and synthesis, but don’t mistake that for deep, human understanding.

- Reward learning and experiences that customers trust.

And I know, I know. Another AI story. But it’s here to stay and around us at all times. I believe that if we approach it with indifference, we remove the emotional component. We can look at it coldly and best determine how it best fits into our processes.

Four Stories. One Pattern.

Diesel and labor volatility hitting summer margins. A rare earth supply chain that’s finally diversifying after years of trying. Berkshire betting on homeownership at a time when the data say the dream is fading. AI generating faster experiences that customers say aren’t better.

Different sectors, different impacts. There is a universal thread, though.

The old assumptions are being tested. The companies doing the quiet work of stress-testing their own setups (their supplier maps, their carrier relationships, their pricing models, their customer journeys) are the ones who will be successful for themselves and their partners going into the back half of the year and beyond.

What’s getting tested in your operation right now?

Bonus #1: Here Comes the Sun(screen)

With all the extra sunshine this time of year comes a real risk of sun damage. I read Katelyn Jetelina’s sunscreen primer at Your Local Epidemiologist this week, and it’s a useful refresher heading into the season.

A few highlights worth keeping in mind:

- Broad-spectrum, SPF 30 or higher; reapply every two hours when you’re outside. More often if you’re swimming or sweating.

- Mineral vs. chemical sunscreen? Bottom line… both work. Choose the one you’ll use.

- Don’t forget your hands, your ears, your scalp if it’s exposed, and the back of your neck when you’re driving. Skin cancer rates are notably higher on the driver’s-side arm and face in the U.S. for exactly this reason.

Full disclosure, reading public health writing hits a little different in your 50s than it did in your 20s. Apply liberally. And, I can’t help myself. We made things in the 80s and 90s. When it comes to sunscreen, my mind invariably returns to this…

Bonus #2: Toys My Grandfather Played With

Speaking of making fun stuff, here’s a hurtful, ageist headline. HistoryFacts ran a piece this week on dangerous toys that have since been banned, and I had to confront the fact that I played with a couple of the toys on this list.

Lawn darts. Easy-Bake Ovens (which, it turns out, caused some genuinely terrible burns). The Atomic Energy Lab, which shipped with real radioactive samples. Aqua Dots, which metabolized into GHB in the body and put kids in comas. CSI fingerprint kits, with actual asbestos in the powder. The list goes on. And on. Plus, somehow my Instagram feed is getting populated with AI videos of things we used to do in the day – “the golden age of childhood endangerment.”

Worth a read for the nostalgia, the mild horror, and the reminder that we have gotten safer in some genuinely important ways.

You’re welcome.

Remember, it costs nothing to be kind.