By Alex Stark

The Squeeze—What Tariff Price Hikes, a 2% Economy, the Carrier Capacity Crunch, and a Wharton AI Study All Have in Common

The calendar says May. The weather outside my window in northeast Pennsylvania says early April. The trees are just starting to bud, the overnight temps are still flirting with frost, and the forecast tells me below-seasonal highs are going to keep me in a fleece for at least another week. At 1,400 feet above sea level, you learn to take the East Coast spring memos with a grain of salt. We run about a month behind our friends in the Philly and NYC areas.

It’s a useful metaphor. Sometimes the calendar tells you one thing and the conditions on the ground tell you another. You can either pretend it’s May and freeze or dress appropriately for the outside temperature.

This week’s reading was a master class in that exact disconnect. Four different stories, consumer prices, the U.S. economy, the trucking market, and an AI study out of Wharton, yet they all pointed at the same thing:

Pressure is showing up everywhere. The temptation is to reach for clever new tricks. The data says reach for the fundamentals.

Here’s what I mean.

1. Where Americans Are Drawing the Line on Price Increases

After a brief pause during the holiday season, a new round of price increases is rolling through the economy, and consumers are pushing back in ways that should matter to anyone running a B2C or B2B operation.

A few data points worth marinating on:

- Companies absorbed most of last year’s tariff impact. Now those costs are being passed through, with high single-digit price increases on everything from jeans to spices to housewares.

- American consumers and businesses are paying roughly 90–96% of recent tariff costs (per the Kiel Institute and Tax Foundation), not foreign exporters.

- Tariffs cost the average household ~$1,000 last year and are projected to hit ~$1,300 in 2026.

- The “K-shaped economy” keeps widening. For roughly a quarter of lower- and middle-income households, rent now eats more than half of annual income. That’s up from about 20% from 2019.

Last week, I wrote about Tillster’s finding that 45% of consumers said their favorite restaurant brand changed in the last year (a 12-point jump from the year before). This week’s WSJ data tells you why. The cumulative tariff drag, plus a fresh round of price hikes, is pushing households to re-evaluate every recurring purchase. The “stickiness premium” you used to enjoy from inertia and brand familiarity is gone.

If you’re a B2B vendor, here’s the chain reaction worth thinking long and hard about. Your customers’ customers are squeezed, which means your customers are squeezed, which means your renewals this year will be tougher than last year. Even if your product hasn’t changed.

The practical takeaway? Audit every line item where you’ve raised prices in the last 12 months. Then (if you can) audit every line item where your competitors have raised prices in the last 12 months. The gap between those two lists is either your opportunity or your warning sign.

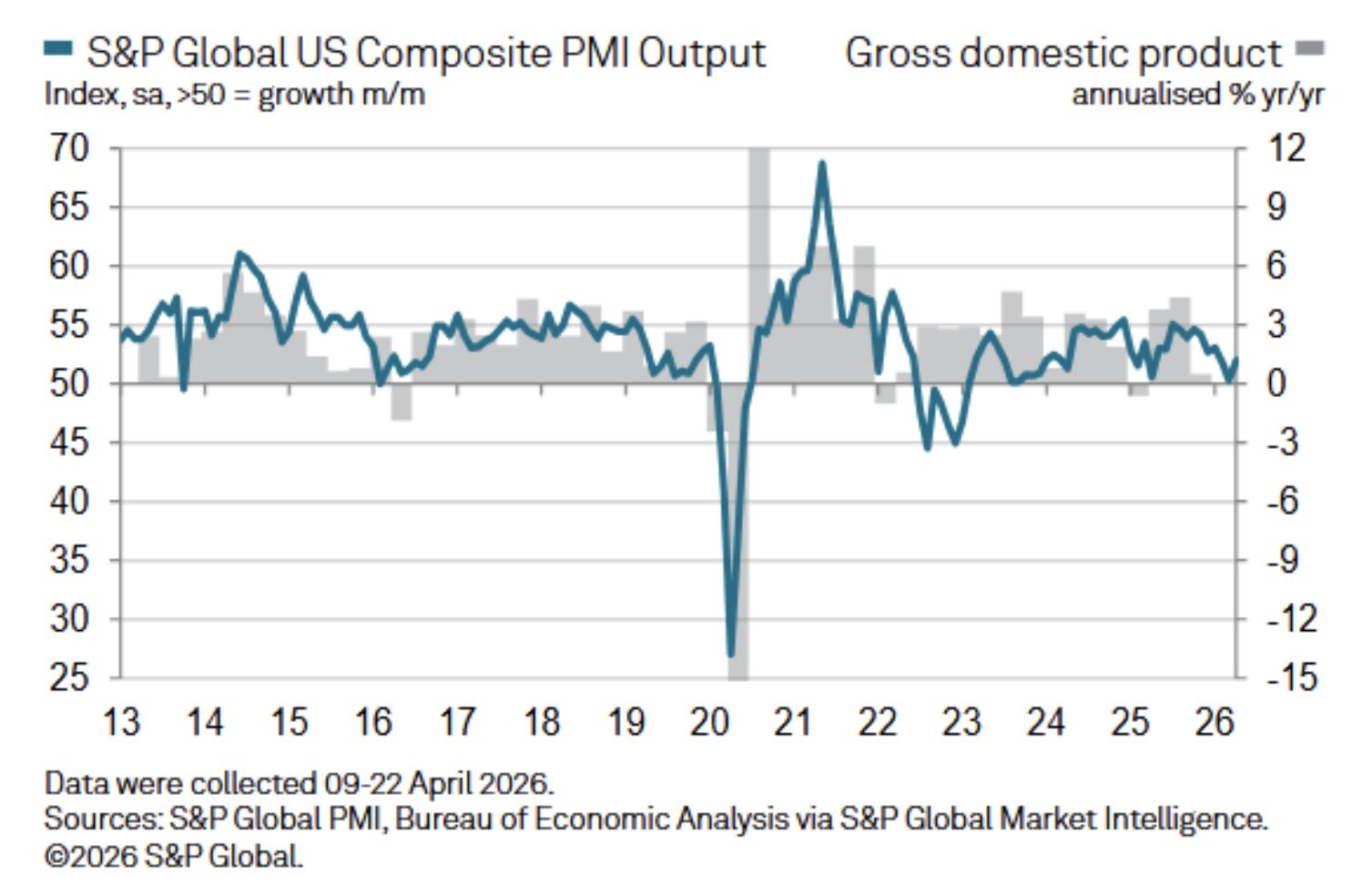

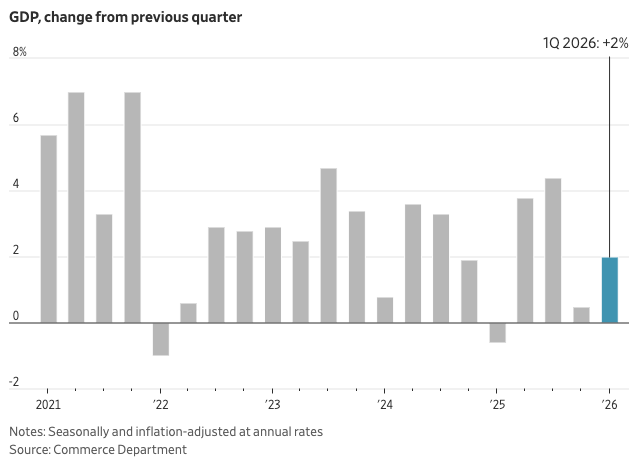

2. The 2% Economy: A Rebound with Wartime Asterisks

Q1 2026 GDP came in at 2.0%, which is a real rebound from Q4 2025’s anemic 0.5%, which was hammered by the 43-day federal government shutdown last fall. On paper, that’s good news. In practice, almost nobody is reading this number cleanly because the Iran war started mid-quarter.

The Numbers Underneath the Headline

- Federal government spending grew at a 9.3% annualized rate, contributing more than half a percentage point to growth.

- Consumer spending growth slowed to 1.6%, down from 1.9% in Q4.

- The “core” measure (consumer spending plus private investment) grew at 2.5%, accelerating from 1.8%, so it seems that the underlying private economy is holding up.

- PCE inflation ticked up to 3.2%, well above the Fed’s 2% target.

- EY-Parthenon now forecasts 1.8% GDP growth for the full year, which is a slowdown from 2.1% in 2025.

There are two honest readings of this data, and I think serious operators need to plan for both.

Here’s the optimistic read. The U.S. economy is more resilient than the headlines suggest. AI investment is genuine. The Q4 weakness was a one-off government shutdown. Underneath the noise, businesses are still spending and hiring.

But the pessimistic read. Government spending is doing a lot of the heavy lifting. Consumer spending is decelerating. Inflation is running above target. And the war in Iran is going to take a real bite out of the rest of 2026 through energy prices and broader uncertainty.

Carl Weinberg, chief economist at High Frequency Economics, captured this moment perfectly:

“The truth is that we do not have any defensible basis for trying to project how these indicators will print.”

When professionals openly admit they’re flying blind, that’s a tell. Run two budgets for the second half of 2026: one assuming the current trajectory holds, one assuming a 50–75 basis point hit from energy prices and consumer pullback. The companies that got caught flat-footed in 2008 and 2020 were the ones that planned for a single scenario. Don’t undervalue the power of being nimble.

3. Why Shippers Are Running Back to Asset-Based Carriers

Werner CEO Adam Miller said something on the company’s Q1 earnings call that got picked up in Supply Chain Dive this week and is worth a hundred trade-press headlines. Shippers are aligning more aggressively with asset-based carriers because spot market discounts have evaporated, and regulatory enforcement is squeezing capacity out of the market.

What’s Actually Happening in the Freight Market

- Tender rejection rates have stayed above 14% for parts of 2026, according to a joint Sonar/Ryder report.

- Shippers are issuing off-cycle “mini-bids” not to lower prices, but to secure capacity.

- The English language proficiency enforcement order has driven significant capacity out of the trucking market.

- Several carriers have already filed for bankruptcy in 2026, including STG Logistics, NAS Logistics, and Bound Logistics.

DAT iQ’s Dean Croke nailed the reframe earlier this year, and I haven’t been able to stop thinking about it:

“Shippers aren’t buying a discount. They’re buying risk.”

That one sentence should be printed and stapled to every transportation procurement strategy this year. When you take a low spot rate from a non-asset carrier with a thin balance sheet, you are not saving money. You are financing your own capacity uncertainty. The bill comes due exactly when you can least afford it, during peak season, a weather event, or a regulatory shift, take your pick.

Reliability Is the New Pricing Power

This is a story that a lot of us in asset-based logistics have been waiting for the market to figure out. Owned equipment, owned drivers, and owned process discipline aren’t “nice to haves.” They’re the difference between a shipment that moves and a shipment that doesn’t. The market is finally pricing that in.

Holman has built its 162-year story around that simple idea: the partner you choose matters more than the rate you negotiate. Asset-based carriers don’t disappear during downturns. They are built to weather them. If that’s a conversation worth having for your operation, our service philosophy lives here.

4. Stop Asking Your AI to “Act Like an Expert”

If you’ve attended any AI productivity webinar in the last two years, you’ve heard some version of this advice: “To get better answers, tell the model to act like a world-class [insert profession here].” Senior Python developer. Board-certified oncologist. Tax attorney. Marketing executive. Whatever you need.

If you’ve attended any AI productivity webinar in the last two years, you’ve heard some version of this advice: “To get better answers, tell the model to act like a world-class [insert profession here].” Senior Python developer. Board-certified oncologist. Tax attorney. Marketing executive. Whatever you need.

It turns out that advice is… wrong. Or at minimum, much weaker than promised. New research from Wharton’s Generative AI Labs tested six major large language models against roughly 500 PhD-level questions in science, engineering, and law and found that expert personas delivered no consistent boost in accuracy and, in some cases, made results worse.

A few specifics from the study:

- Telling the model to respond like a “toddler” cut accuracy in four of six models. (Funny, but instructive.)

- Assigning the wrong type of expert role sometimes degraded performance noticeably.

- The persona prompt occasionally pushes the model toward the failure modes of expert communication, which can be overconfident, jargon-heavy, and occasionally wrong.

Researcher Lennart Meincke summed it up bluntly:

“AI is not super reliable. Ask the same hard question 25 or 30 times and you only get the right answer a few times.”

So what actually works?

According to the Wharton team and a similar Carnegie Mellon study from earlier this year, the gains come from how you frame the task, what context you provide, and how you check the output. Not from layering personas on top of prompts. Personas are useful for tone and presentation. They’re not magic accuracy boosters.

The Workforce Mismatch Underneath All This

This dovetails uncomfortably well with another finding I read this week. A Skill Dynamics survey found that 92% of supply chain organizations have at least one critical skills gap in their workforce, with AI being the most prominent. The catch? 83% of those organizations also said they felt “at least somewhat prepared” to leverage AI, while simultaneously admitting they lack the actual skills to use it effectively.

Confidence isn’t capability. Maybe part of the gap is that we’ve been training people in prompt-engineering tricks that don’t actually work, rather than on the fundamentals of framing tasks, providing context, and checking outputs. Imagine that.

Bringing It Together… The Squeeze

Every story this week pointed me in the same direction.

- Consumers are squeezed and pulling back from brands that used to be safe.

- The economy is squeezed, growing, but with a wartime overhang and inflation back above target.

- Carrier capacity is squeezed, and shippers are paying more for reliability instead of less for risk.

- Workforce skills are squeezed, and the AI tricks people learned aren’t the ones that work.

The temptation in moments like this is to reach for clever new tactics. A creative pricing scheme. A novel routing arrangement. A magic prompt. The data this week argues for the opposite. Go back to fundamentals. Clear pricing. Being reliable. Real skill development. Real prompts that say what you actually want.

One hundred and sixty-two years of doing this teaches you something quietly important: every “we’ve never seen anything like this” moment looks roughly the same as the last “we’ve never seen anything like this” moment. The fundamentals work because they always work.

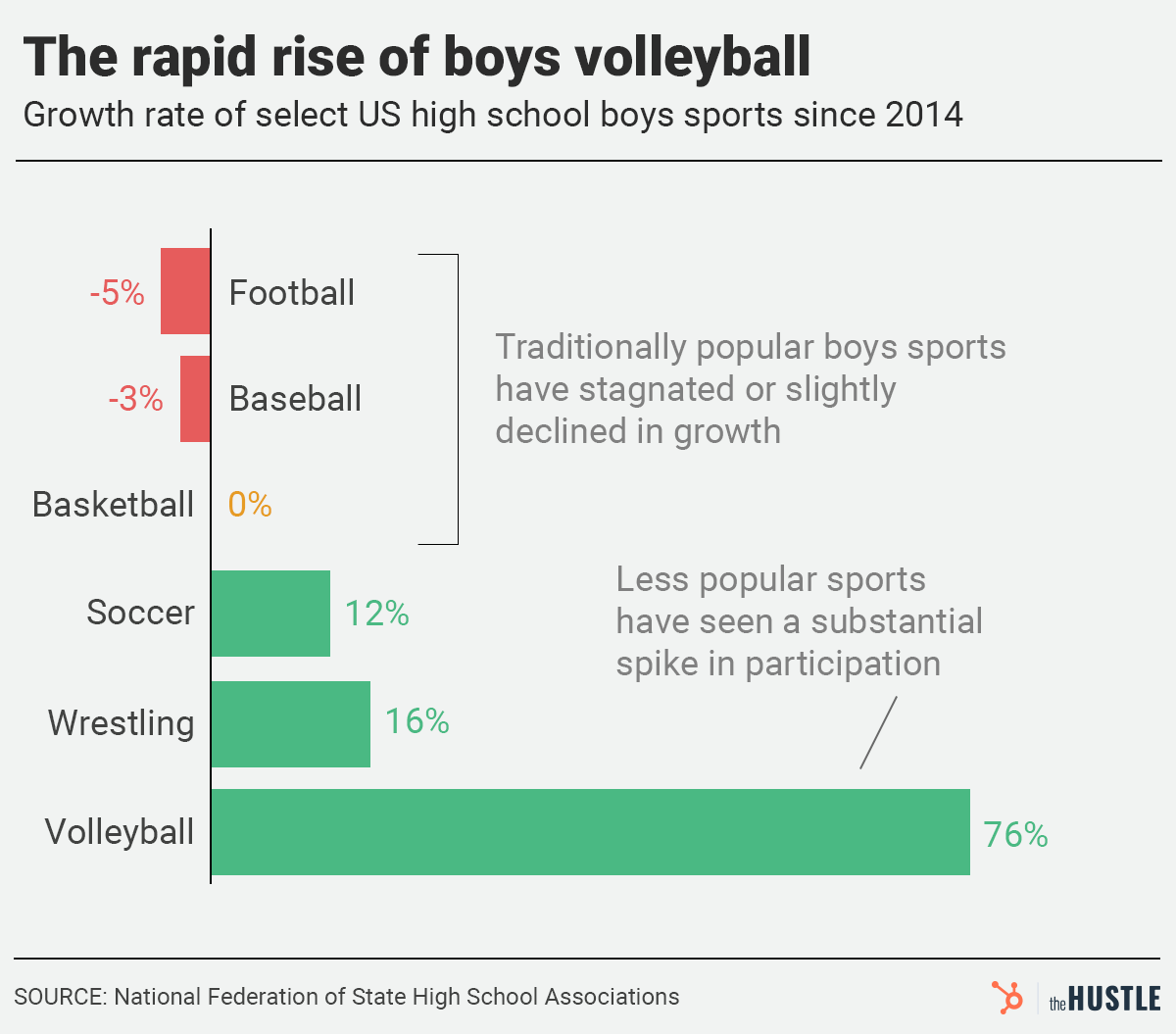

Bonus #1: Can Men’s Volleyball Save American Colleges?

An interesting piece from The Hustle this week about a different kind of squeeze most of us aren’t watching. Small private colleges are facing a “demographic cliff” as the 18-year-old population shrinks. Their unexpected lifeline? Niche sports. Schools like Hartwick (Oneonta, NY) and Newberry (South Carolina) are launching men’s volleyball, women’s flag football, and other lesser-known programs to attract athletes who pay tuition.

Fairleigh Dickinson calculated that adding men’s volleyball costs $350K a year but generates $470K in tuition for a net positive of $120K. That’s not athletics. That’s an enrollment strategy.

The supply chain analogy is too tempting to ignore.

Sometimes you don’t need a flashier version of what everyone else has. You need to find a category nobody’s bothered to optimize.

Bonus #2: One Last Thing… The Sears Catalog

This one’s pure nostalgia. History Facts ran a piece on 10 bizarre things you could once order from the Sears catalog. I’m old enough to remember that beloved catalog arriving at our house before Christmas and being completely enthralled. I feverishly flipped through every page, kept it away from my younger sisters, dog-earing the corners, building a wish list (Santa!?) nobody was going to fulfill.

Mail-order kit houses. Electric belts. Tombstones. Even heroin (yikes). The Sears catalog was wild. For generations, it was the supply chain. It was the everything store before the everything store. There’s a whole logistics nerd’s history of distribution embedded in those pages.

It’s a rabbit hole worth a couple minutes of your day.

You’re welcome.

When the Squeeze Is On, Choose a Partner Who’s Built for It

At Holman Logistics, we’ve spent 162 years being the asset-based partner shippers turn to when reliability matters more than the rate sheet. If your team is rethinking its transportation strategy in a market where capacity, cost, and certainty are all moving in the wrong direction, let’s start a conversation.

Remember, it costs nothing to be kind.