U.S. Domestic Economic Items

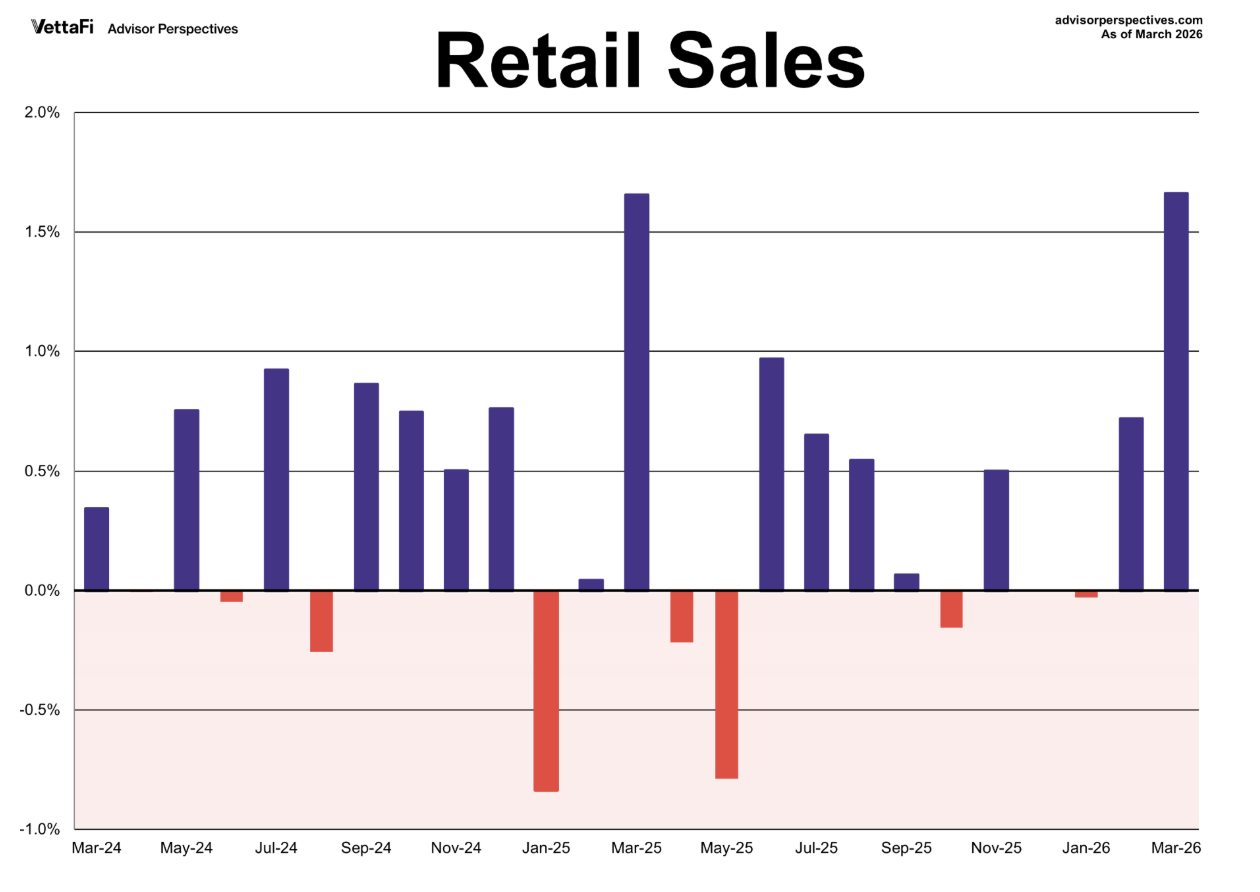

If there were a canary in the coal mine to watch, it would be the monthly Advanced Retail Sales data, and the canary is still singing. It was a strong report, almost across the board. Top-line growth was strong at 4.0% Y/Y; even after stripping out the impact of food and fuel, it was up 4.2% Y/Y.

Even after adjusting for inflation, retail sales were still up 0.7%. Whether this will hold in the coming months under the weight of higher fuel prices is another question.

Gas station retail sales, up 18% Y/Y, were all price-driven. Gasoline is actually modestly elastic. When prices go up, demand eventually softens. That said, people still have to get to work and school. But we see more carpooling and less pleasure driving, etc., in some household income categories, which softens total gasoline demand.

According to the report, there was a pullback in some higher-ticket discretionary categories (though not all), such as automotive and furniture.

Yet the strength of the consumer probably showed up most clearly in discretionary spending categories. For instance, electronics and appliance stores got the tax refund boost. We also saw a surge in clothing and sporting goods, and even a few signs of life in department store sales.

What we need to watch is whether this tax refund incentive is a sugar high or something sustainable.

Possible Petrochemical Supply Shock

This is something worth keeping an eye on for downstream price impact.

There appears to be a building-supply crisis for polypropylene (PP) and polyethylene (PE) that can be traced directly to the disruption of the Strait of Hormuz. The Persian Gulf corridor handles approximately 20% of global seaborne crude oil and a disproportionately higher share of global petrochemical feedstock exports, specifically naphtha, ethane, and propane, the primary building blocks for PP and PE production.

Chinese petrochemical producers, who collectively account for the world’s largest purchases of PP and PE, are simultaneously facing higher feedstock costs and tighter feedstock availability.

The result is a cost-push inflation surge at the most upstream point in the polymer supply chain, one that is now working its way downstream through every product category that contains plastic content.

Read this week’s Brief for more market insights.