Producer Price Index Sending Mixed Signals

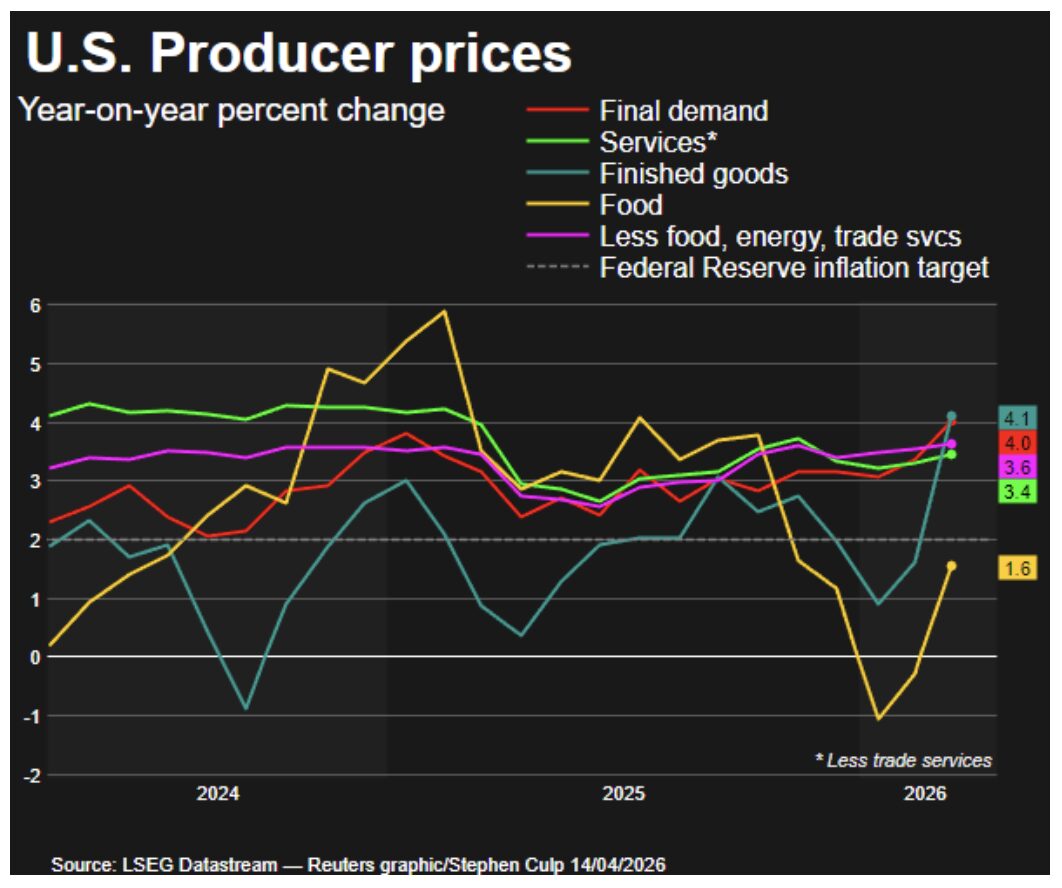

We mentioned “false flags” in last week’s report. The Core Producer Price Index (PPI) measures average price changes received by domestic producers for their output, excluding the volatile food and energy sectors. The measure serves as a predictor of consumer inflation (CPI) by tracking price changes at the wholesale level.

Currently, U.S. Core PPI inflation is showing signs of easing, with a March 2026 monthly increase of just 0.1%. That is below the expected 0.5% forecast and lower than in previous months.

Year-over-year, Core PPI is at 3.8%.

There are indications of easing; however, a higher-than-expected Core PPI often suggests persistent, cost-driven inflation, which can lead to higher interest rates and likely arm the Fed to cite these ratings as grounds for opposing a rate cut.

The bottom line is that the impact of the conflict on Producer Prices still appears to be working “upstream.” It hasn’t yet reached the OEM or Tier 1 supplier level. Results and news on that would likely surface later this month or in May.

Still, it’s a warning sign to watch your supply chains.

U.S. Domestic Economic Items

National Association of Home Builders (NAHB) sentiment tanks. Perhaps that should have been expected.

Surprisingly, the “least worst” sector was the northeast, with a 2.4% M/M decline and a 4.7% Y/Y drop. Followed by the south, which was not a surprise. But even in those markets, there is a notable decline in sentiment between March and April.

Second, sentiment for the next six months is slightly better than expected. It was down just 2.3% over last year at this stage. Maybe there is a possible scenario that still reaches 4-5% growth.

For now, homebuilders are riding the storm out and watching for some relief. The concerns are a trifecta:

- Higher bond rates are pushing mortgage rates higher.

- Higher raw material and labor costs.

- Supply chain issues – can they get the materials that they need when they need them? Or should they expect stockouts of certain materials?

There is a lot to be worried about. But again, there are some conditions and efforts underway that could turn this around quickly.

Read this week’s Brief for more market insights.