Rethinking How to Predict Recessions

The government shutdown has given those at the Federal Reserve some time to think, research, and do some overdue analysis of data. Rather than focus on their daily scramble to get data cranked out, they’ve had time to sit back and take a deep dive into different types of analysis.

The Cleveland Fed does some great economic work, and they looked at the role of regional economic sentiment (vs. national sentiment) in predicting recessions. What they found was that using some weighted indexing and regional sentiment (typically shown in the regional Beige Book data) was more accurate in predicting recessions.

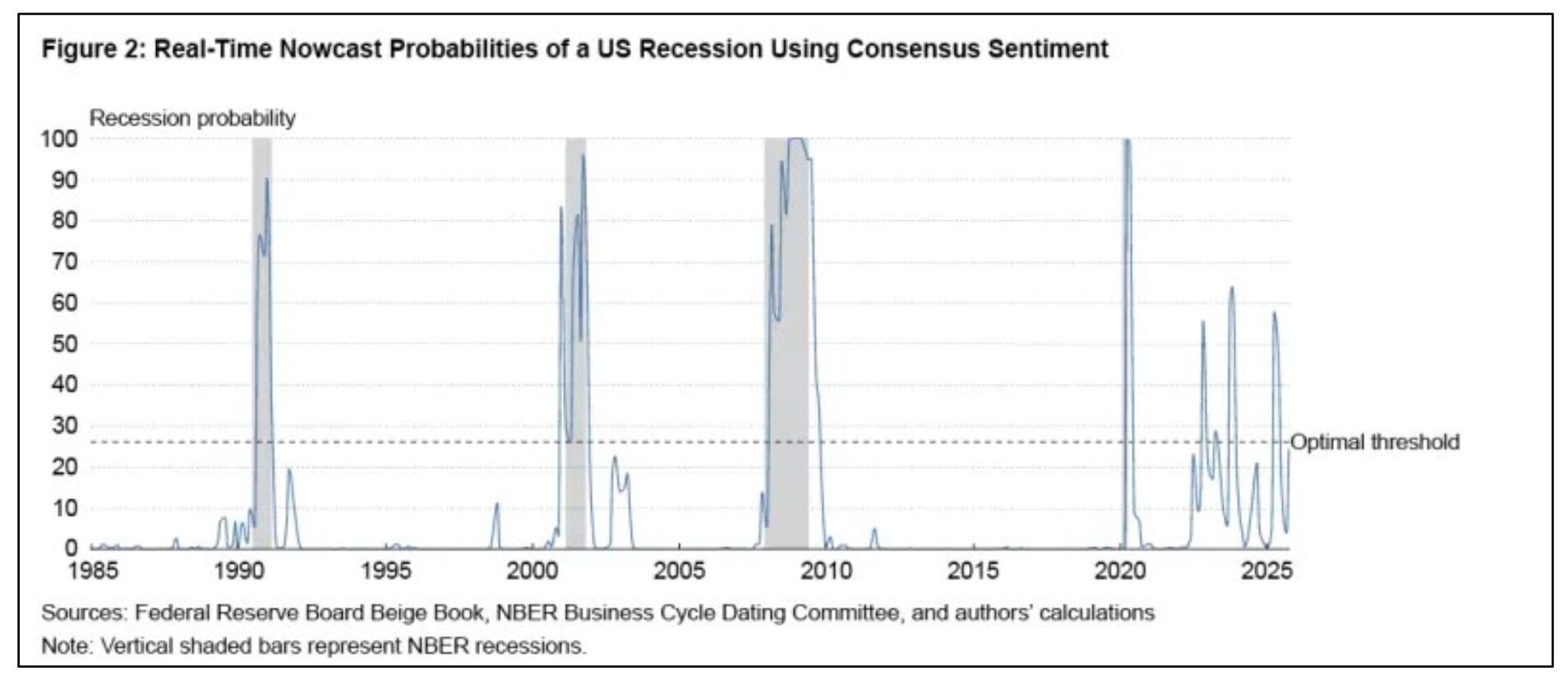

The chart below shows the new real-time forecast for recession risk, and it shows that historically it has been perfect in predicting recessions and since the pandemic – it is batting zero. The Cleveland Fed officials even made a similar comment, that the pandemic (being a 100-year event) potentially will force us to rethink many traditionally accurate measures or it will take time for economic systems to return to their prior relationships. This period is exacerbated by historic retirements (allowing many people to exit the workforce), great wealth transfers, work-from-home, technology and automation factors, and other issues that make this recovery from the pandemic…different.

The recession probability index is still sitting at about 25%, despite US GDP and other figures showing that the US is out of recession risk. But note that in 2022, the probability shot up to nearly 65% and it revisited those levels earlier this year. The risk level needs to go much higher, back into the 50-60% range, before anyone can realistically signal that recession is imminent. But its current levels are worth noting.

At this point, the biggest take-away is that this is an important informational tool to keep an eye on, but it isn’t the only one. Given its performance in the past couple of years, there is no reason to worry that a recession is imminent. In addition, some recessions are short and shallow, and many industries don’t even realize it. The current market probably doesn’t need a sharp reset – and there are several mechanisms that can pull it out quickly or head it off entirely (the Fed has a lot of room to trim interest rates) and the Treasury is building some headroom (slowly) to help fight a recession.

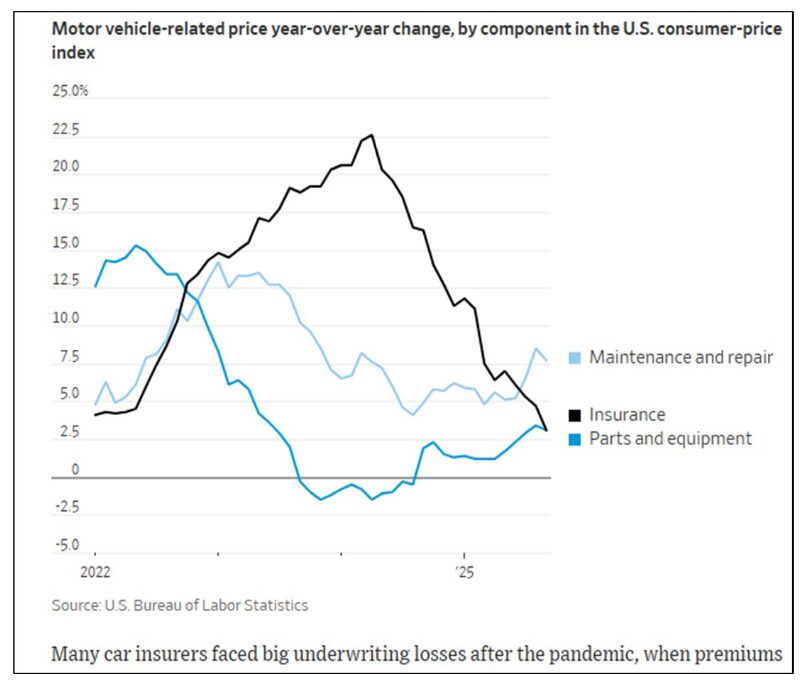

Competition Catching Auto Insurers?

Competition Catching Auto Insurers?

Looking at auto insurance inflation, it has fallen to the lowest annual rate of growth in many years. Prior to the pandemic, the average annual rate of growth was nearly 3%, and damage was done with it surging by 55% over the past 5 years. Competition, vehicle safety, and lack of national disasters the past year (mostly lack of hurricane damage), have helped pull premiums down for privately insured vehicles. On the inflation front, this helps.

Univ. of Michigan Consumer Sentiment Weakens

Expectedly, the consumer sentiment reading early in November was weak – the weakest since 2022 (during the early stages of the Russian invasion of Ukraine). Sentiment could remain weaker heading into the holidays. Even with the government reopening, there are still other concerns in the economy that consumers are dealing with. Inflation is still top of the list of concerns, and increasing concerns over layoffs are also now playing with sentiment. However, sentiment can rebound quickly, so this is simply a partial-month snapshot. Read MORE.