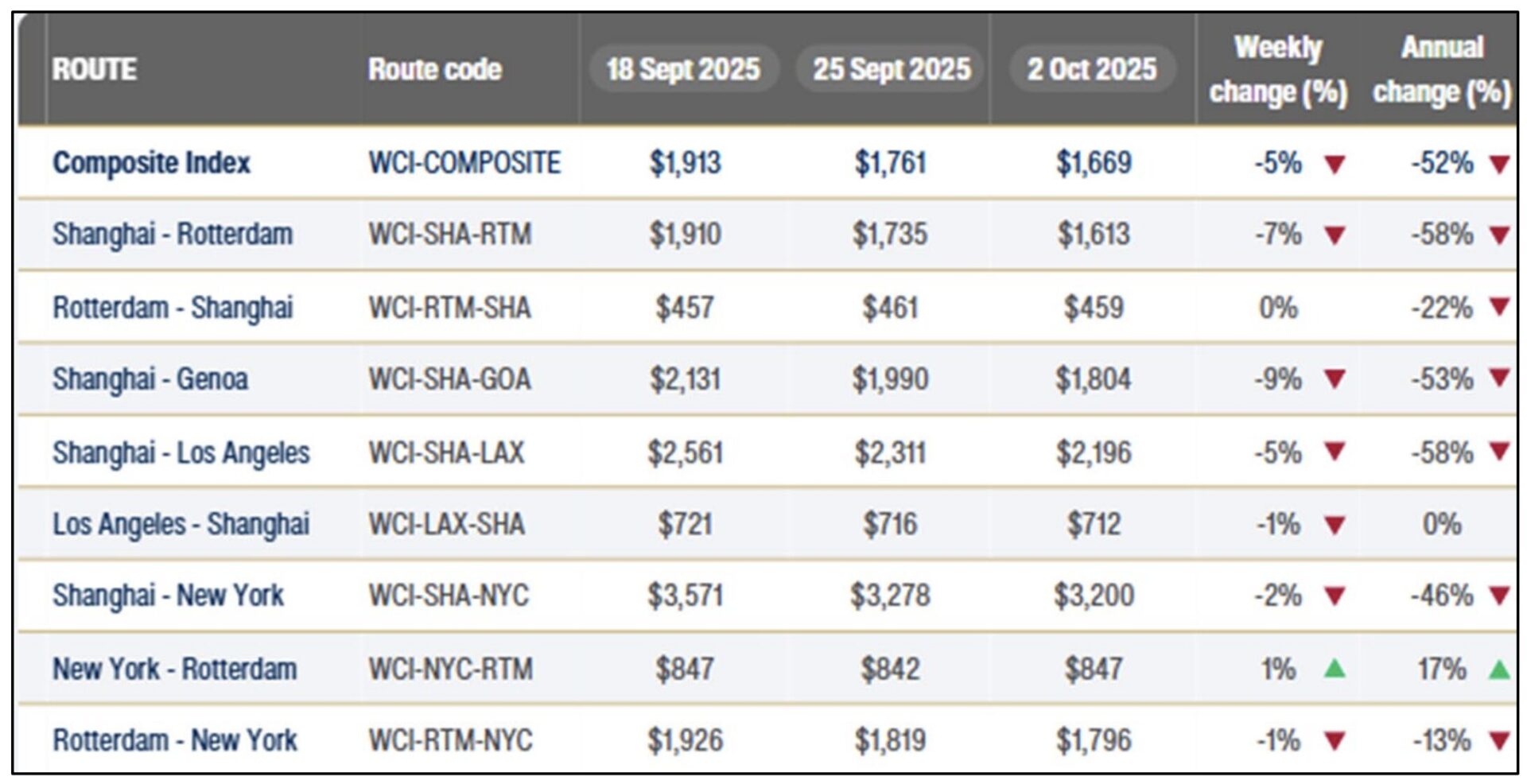

Still No Freight on Water

There were hints that trucking activity might be picking up, but there still isn’t any “freight on water.” The Drewry container price indexes through October 2nd showed that most of the metrics were still down year-over-year, and there just isn’t anything headed this way.

This is a checkpoint, not a full report. The data shows that inbound cargo headed to the US West Coast from Asia is still down 58% from where it was a year ago. And although this is a price- based measure, it is based largely on supply-demand metrics – and with prices falling, it shows that there just isn’t any demand.

This is a checkpoint, not a full report. The data shows that inbound cargo headed to the US West Coast from Asia is still down 58% from where it was a year ago. And although this is a price- based measure, it is based largely on supply-demand metrics – and with prices falling, it shows that there just isn’t any demand.

For those lanes looking at Asia to US East Coast, the same story holds with prices being down 46% Y/Y.

Even when one looked at sequential weekly movements in price, there weren’t any increases being witnessed in the spot market.

Keep in mind that these measure spot rates, and most cargo moves by contract rates. But to the degree that spot rates give us a glimpse into supply/demand dynamics, it is a valuable insight.

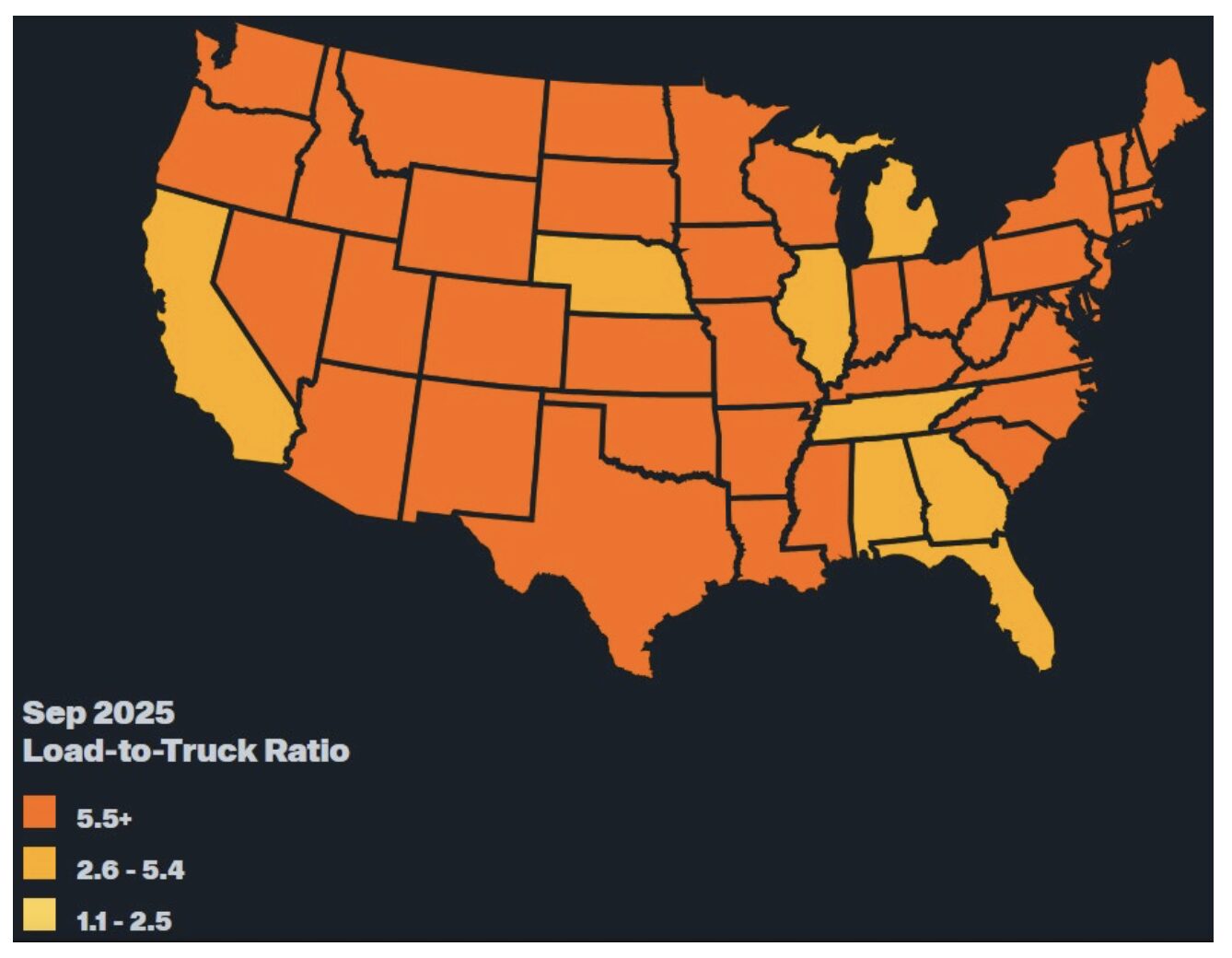

Harvest Season Hits Trucking

One of the sources (and there are many of them) that help track weekly trucking activity is DAT Trendlines – and they publish public aggregated data on current load-to-truck-ratios (LTR). This is the number of loads for every available truck. And when this metric is higher, capacity is tighter.

The map below from DAT shows the recent LTR national map and states with the dark orange are the highest level of capacity tightness.

Right away, one sees that many states that have heavy agricultural production are the tightest as harvest season kicks into higher gear.

But offsetting that is a lack of activity at critical port areas. Georgia and California specifically are seeing slack capacity in most of their markets. Depending on what type of transportation you are purchasing, some driver capacity is tight across many of these markets, and this diversion of driver capacity from the dry-van truckload sector to the ag commodity-based movement is evident and important.

In the past few weeks, prices have inched up only modestly. It is still a weak signal overall, and there still remains too much capacity in the TL market at the moment (given the current volume of dry-van demand out there). Cold chain activity is still strong; the LTR for refrigerated transportation is showing an increase in the number of loads looking for trucks in just the past few weeks (it was up 118% Y/Y through the end of September!).

Again, the bottom line is that prices have not yet started to recover, but other elements that create the tendency for price escalation are in place. The thinking is that the country will get through harvest season, and then the LTR will fall off a cliff.

Axios Sends Up Caution Flare on Labor Survey Data

Axios’ latest data shows “job market gloom” at its highest levels since the Great Recession, with pessimism centered on several key segments: entry-level workers, younger adults, and small businesses. About 62% of Americans surveyed in August 2025 believe unemployment will worsen in the coming yea —matching the levels of fear seen during the 2008 financial crisis.

On a closer look, one learns that 1) AI is a factor, and current automation efforts are affecting entry-level jobs. But 2) it also pointed out, the percentage of “job-huggers” is surging (people working to hang on to their current job). Federal data shows that it might not be that dramatic, but private surveys are showing something different. Employees may need some reassurance.