U.S. Domestic Economic News

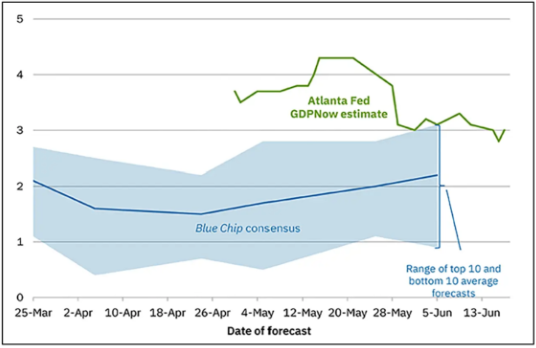

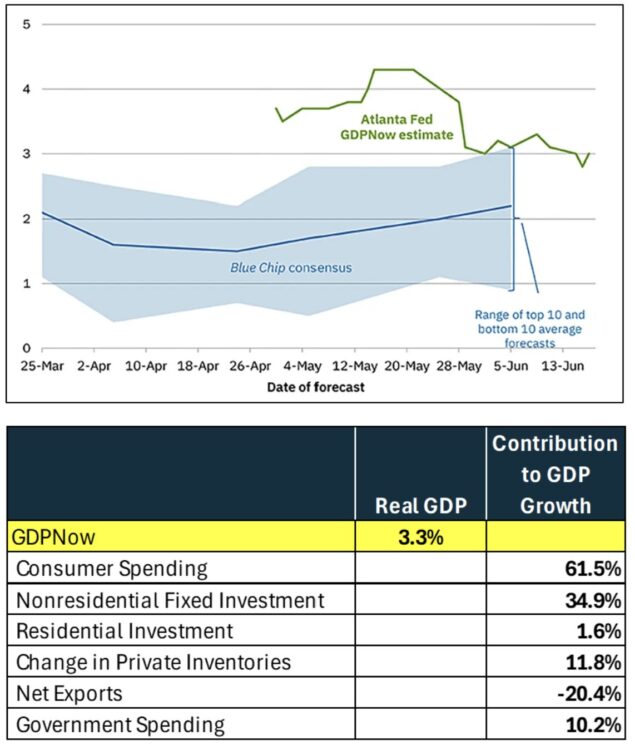

The latest data in the Atlanta Fed’s GDPNow tracker show it trending at 3.04% for Q4, which is a healthy growth rate. But as usual, we want to break down the components of GDP driving growth to provide granularity on where growth is strong and where it might be stalling.

The chart below from the Fed shows the path of GDP through the quarter, with GDP ticking up after dipping to 2.8%. The latest retail data helped bump it up to 3%.

Blue Chip analysts are still looking for growth somewhere in the 2.2% range, but even their forecasts have been inching up since the beginning of the quarter.

The bigger story is the composition of GDP growth. The other table below shows the various components and their contribution to Q2 growth rates. Consumer spending is (and always will be) the biggest contributor to GDP. The percentage changes over time, but at 61.5%, the U.S. consumer is carrying just about the normal weight of GDP growth (~60%).

Fed Shocker… But Only in a Statement

The Fed’s action this week didn’t come in what it did or didn’t do; it’s in what it didn’t say.

It really didn’t say anything. The statement from the Federal Reserve was pared down dramatically and offered almost no forward guidance. What analysts and the stock market picked up on was that the tendency to lower rates was all but replaced by a tendency to increase rates perhaps later in the year. In other words, a rate cut is probably off the table for now, while a rate hike may be in the cards – although they didn’t say that.

All the Fed statement generally said was:

- Employment was stable

- Growth was reasonable, and

- Inflation was still too hot.

Read more on how today’s news and other global items are affecting the supply chain.