By Alex Stark

What We Built vs. What We Need Now: Why the Protein Boom, Negative Real Wages, the Saudi Truck Convoy, and a 1,500% Cargo Theft Surge Are All the Same Story

It’s been a relentless week for industry news, or all news for that matter. I had so many tabs open (across multiple browsers) that I was likely redlining my RAM. By Thursday, after a refreshing morning run, I saw the pattern and wrote what I was thinking:

A lot of what we built for the past 30 years quietly assumed a stable world. We didn’t build for resilience because we didn’t need to. Now we do.”

That’s this week’s thread. I quadrangulated around four very different stories. The first is the protein supply crunch. Next, real wages turn negative amid inflation. Followed by a convoy of 3,500 trucks barreling across the Arabian Desert, and our federal government finally noticed a 1,500% surge in cargo theft. All four articles point to the same insight from different angles.

Here’s what I mean.

1. The Protein Boom Is Breaking Dairy’s Production Math

Protein everything, everywhere. It seems that consumers can’t get enough. Whey protein concentrate, which for decades was treated as a cheap byproduct of cheese manufacturing, has become one of the most in-demand ingredients in the U.S. food system. Food Dive reported this week that standard whey powder prices have risen more than 50% since January, and some suppliers are sold out through the rest of 2026. BellRing Brands (the parent of Premier Protein and Dymatize) called whey prices “historic highs” on its latest earnings call.

Forces Behind the Shortage

- 70% of Americans now say they want more protein in their diet, up from 59% four years ago. Protein has migrated from the supplement aisle into Pop-Tarts, Kraft Mac & Cheese, and even Doritos.

- GLP-1 medications like Ozempic and Wegovy have created an entirely new category of protein-dependent consumers. Some people are eating fewer calories overall and looking to protein to fill the gap.

- U.S. cow milk has lower protein content than milk in other countries, partly due to genetics. That limits how fast domestic production can scale.

- $11 billion in new manufacturing capacity has been announced across 19 states, but new processing facilities take years to come online. Meaningful supply relief isn’t expected until late 2026 or 2027.

Here’s the part that grabbed me. As dairy producers ramp up whey output, they’re also producing more butterfat as a parallel byproduct. However, that surplus has driven butterfat prices down, creating volatility on the other side of the cow’s economic ledger. Optimizing for one output is quietly breaking the economics of the other.

This is the clearest illustration I’ve seen of the week’s theme. For 50 years, the U.S. dairy industry built its production economics around cheese as the main product and whey as the byproduct. When consumer demand reversed, and whey mattered more, the system couldn’t pivot quickly.

The infrastructure was efficient for the world that was, and isn’t for the world that is.

The takeaway is that every “byproduct” in your operation is one trend away from becoming your most profitable product or service. Audit the leftovers the way you audit the main products. The market sometimes flips them on you.

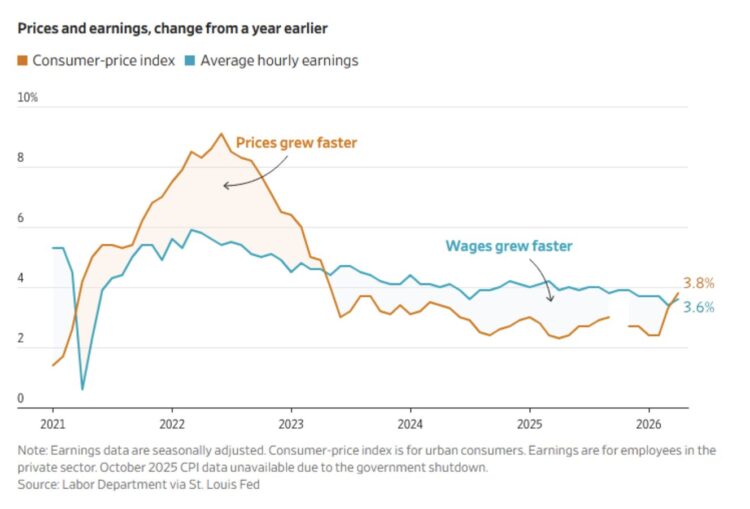

2. Real Wages Just Went Negative for the First Time in Three Years

April’s CPI came in at 3.8% year-over-year. That’s the highest reading in nearly three years, as stated by Retail Dive’s reporting this week. Wage growth came in at 3.4%. For the first time since May 2023, inflation is outpacing wage growth. The retail, restaurant, and CPG industries just lost their tailwind.

What’s Pushing It

- Energy costs from the ongoing Iran conflict (gasoline and diesel)

- Shelter inflation is running at 3.3% annually

- Food prices are climbing on the back of input cost pressures (see Point #1)

- Core CPI is still elevated at 2.8%

Here’s the structural assumption that’s being tested. For three years, retailers, restaurants, and CPG brands built pricing strategies on the premise that nominal wage gains would absorb price increases. Customers might grumble, but they could pay. That premise has just broken.

This connects directly to the WSJ tariff data I wrote about a few weeks ago. Households are now absorbing roughly $1,300 a year in cumulative tariff costs, according to Tillster CX research, which shows that 45% of consumers said their favorite brand changed in the last 12 months. Those two stats are no longer a coincidence in light of this recent report. When real wages turn negative, every recurring purchase gets scrutinized.

Follow your right instinct on this one. Stress-test your pricing assumptions against a scenario where consumers have fewer real dollars, not more. Check your customer base for who’s most exposed. Don’t assume the 2024–2025 demand elasticity curves still hold. They almost certainly don’t.

3. The Saudi Logistical Miracle: A 3,500 Truck Detour

Of all the stories I read this week, this one from the WSJ was the one I couldn’t put down. It’s the most operationally vivid supply chain story of the year thus far. And as I’ve opined to my friends and community-based colleagues over the years… Everything comes down to logistics.

When the U.S. and Israel attacked Iran and the Strait of Hormuz disruption began, analysts at the commodities research firm CRU openly questioned whether any Saudi product would get to market. Three months later, the answer is in. Convoys of trucks now move continuously across the Arabian desert between the Persian Gulf ports and Red Sea export terminals. It’s become a mechanized revival of the old camel caravan routes, only this time hauling oil, fertilizer, phosphate, and chemicals.

![]()

The Numbers Are Staggering

- 3,500 trucks are now running continuously between the Persian Gulf and the Red Sea, mostly with two drivers each, and mostly around the clock.

- Truck traffic at the small Gulf of Oman port of Khor Fakkan jumped from 100 a day to 7,000 a day.

- Saudi Aramco has leaned heavily on the East-West pipeline to the Red Sea port of Yanbu. The UAE has pushed more crude through Fujairah.

- Phosphate shipments from Yanbu have now reached Djibouti, Thailand, and Argentina, per vessel-tracking firm Kpler.

Maaden CEO Bob Wilt, who orchestrated his company’s response, captured the whole story in a single quote:

Six hundred became 1,600, became 2,000; now we’ve got 3,500 trucks running from the Gulf to the Red Sea. We didn’t plan for this.”

And then his follow-up, which is the line that really matters:

We’ve demonstrated our capabilities. Let’s harden this and always have a route to the Red Sea.”

CRU’s Peter Harrisson called the whole thing “Saudi Arabia’s logistical miracle.” He’s not wrong.

But the deeper lesson isn’t the miracle. It’s that the miracle was necessary at all.

Efficient and Resilient Are Not the Same

For 60 years, the global oil and commodity system has been optimized around the Strait of Hormuz as the efficient route. It was the shortest path, the cheapest path, the highest-volume path. Nobody built meaningful backup capacity because nobody needed to. Efficient and resilient are not the same thing, and the difference becomes very expensive very quickly once the chokepoint closes.

Every operation has a Strait of Hormuz. A port you depend on. A lane you can’t easily replace. A single carrier, a single facility, a single supplier that handles a disproportionate share of your flow. The system runs beautifully until the day it doesn’t.

When was the last time you actually tested the alternative?

4. Cargo Theft Is Up 1,500%

The U.S. House of Representatives passed the Combating Organized Retail Crime Act (CORCA) this week with bipartisan support, according to Commercial Carrier Journal. The bill, which now moves to the U.S. Senate, would task the Department of Homeland Security with leading a coordinated federal response to cargo theft. The numbers behind the bill are eye-popping:

- $18 million per day is stolen from the trucking industry

- $6.6 billion annually in total financial impact (American Transportation Research Institute)

- Strategic theft is up 1,500% since 2021 (CargoNet)

That last stat is the one that should make every shipper sit up. Strategic theft isn’t pickup-truck-and-bolt-cutters. It’s identity theft and fraudulent documentation used to divert freight rather than physically steal it. Criminals use fake DOT numbers, spoofed broker credentials, social engineering, and digital impersonation to steal entire trailers of freight, and the shipper, broker, and trucker often don’t realize anything is wrong until the load simply never arrives.

ATA President and CEO Chris Spear was blunt about who’s behind it:

Cargo thieves are stealing $18 million every day from the trucking industry, and motor carriers and consumers pay the price. The crimes are often orchestrated by highly organized, technologically advanced transnational criminal groups.”

The Trust Model That Quietly Broke

Our entire freight system was built on a baseline assumption of document trust and identity verification. Tender a load to a carrier. Generate a BOL. Freight moves. End of story. That trust model worked when the bad actors had to physically show up. It’s breaking down rapidly now that the bad actors are digital, organized, and operating at scale.

Even if CORCA passes the Senate, the regulation will lag behind the threat. Shippers and 3PLs need to strengthen their own processes right now by employing tactics such as multi-factor verification for new carriers, secondary identity checks, locked-down digital onboarding, real-time tracking with anomaly alerts, and meaningful escalation paths when something doesn’t look right.

There’s also a structural argument worth making. Asset-based carriers with long-tenured, safe drivers and a stellar track record in the market simply don’t face some of the challenges associated with broker-flipped loads. Fewer, deeper carrier relationships aren’t just about capacity anymore. They’re a risk-management strategy. (We talk about how Holman approaches that here.)

Four Stories. One Pattern.

- We assumed cheese demand would always outpace whey demand. It didn’t.

- We assumed wages would keep up with prices. They aren’t.

- We assumed the Strait of Hormuz would always be open. It isn’t.

- We assumed the identity of a freight carrier was knowable from a DOT number. It increasingly isn’t.

None of those assumptions are wrong on average. They’re wrong at exactly the wrong moments. Unfortunately, the wrong moments are happening more often. Efficiency optimizes for the average case. Resilience optimizes for the bad case. Most of what we built over the last 30 years was optimized for the first one.

The companies that come out of the next disruption ahead are the ones asking these questions…

Where did we optimize for efficiency in a way that quietly assumed stability?

Where do we need to prepare? Not for what’s happening today, but for the next “we didn’t plan for this” moment.

One hundred and sixty-two years of doing this teaches you that the assumptions you can’t see are the ones that hurt the most when they break.

One Last Thing… Develop the Resilience of a Daffodil

A short, lovely piece from Big Think this week argues that daffodils are a worthwhile model for the rest of us. They don’t try to outsmart winter. They don’t try to skip it. They go quiet, conserve their energy underground, and come back when conditions improve. They’ve been doing this for millions of years.

I love this line from the piece: “The wisdom of the daffodil is to recognize that there is something remarkable in submitting to destruction.”

There’s a real lesson in there for any operation that’s been told to optimize relentlessly, always be growing, never go dormant, never pause. Some of the smartest operational designs include dormancy. Think capacity that scales back without disappearing, relationships that pause without ending, or processes built to survive the lean years by knowing how to be small.

Not every system needs to be on all the time. The daffodils figured that out a long time ago.

Call it floral resilience. Pass it on.

You’re welcome.

Built to Weather the Hard Years, Not Just the Easy Ones

At Holman Logistics, we’ve spent 162 years helping shippers see past the obvious move, the spot rate that looks cheap, the optimization that creates a new bottleneck, the assumption that the next quarter will look like the last one. If you’d like a partner who asks the hard questions before disruption forces them to, let’s start a conversation.

Remember, it costs nothing to be kind.